ETX Module: EU ETS over time

The EU ETS is a regulatory market, which means that it is highly dependent on how it is set up, run and changed over time by policy makers. The key document that determines all this is the EU ETS Directive. The three main European institutions (European Commission, European Parliament and Council) are responsible for any major changes and revisions, such as the current one, the Fit For 55 revision.

This revision seeks to bring the EU ETS in line with an increased EU emission reduction target of -55% (up from -40%) by 2030 compared to 1990. This revision (as each one before it) is critical, as it will set the ambition and functioning of the EU ETS for the coming 10 years, a crucial decade for humanity to reign in its GHG emissions. It is part of the Fit for 55 revision package – which contains 15 legislative files, mostly revisions of existing laws, but also introducing some new ones (e.g. the Carbon Border Adjustment Mechanism).

LEARN MORE

Each revision follows the so-called ‘ordinary legislative procedure’, where:

- The European Commission proposes changes to the Directive, after running a stakeholder engagement process which usually incorporates two rounds to gather feedback from stakeholders.

- A first reading follows simultaneously at the European Parliament and the Council. Both institutions determine their position on the revision – they react to the Commission proposal but can each also propose additional changes. This means that each revision of the EU ETS Directive leads to every aspect of the Directive coming under scrutiny and potentially being reopened for negotiations. In theory the European Parliament votes on its position first, and the Council can choose to accept that position (ending the first reading and leading to the adoption of the changed Directive) or adopt a different position (leading to a second reading).

- In practice, however, both institutions adopt their own positions and negotiations start between all three institutions (so-called ‘trilogues’) that aim to reach a compromise text. Estimates for the current EU ETS revision are that by middle of 2022 both Parliament and Council will have adopted their respective positions, with trilogues to start in Summer or Fall 2022. The trilogues could last months to years – as the EU ETS is a political priority and the stakes are high for all stakeholders.

Aside from major changes and decisions (which are made along the lines set out above), the Commission is in charge of the day to day running of the EU ETS. It has been delegated several powers related to the EU ETS, including:

- Detailed arrangements on the auctioning of EUAs

- Running of the central registry which is crucial to the operation of the EU ETS

- Deciding which sectors and subsectors should receive free allocation

- Setting of various technical variables (for example the benchmarks which are used to calculate free allocation to installations)

- Operating the Innovation Fund (discussed more in detail below as well)

- Monitoring of international policy developments (including with regards to aviation emissions, linking with other systems and need for carbon leakage protection)

- Convening specific groups to take technical decisions (for example in the case of ‘excessive price fluctuations’)

In addition to all these responsibilities, the European Commission is also required to report to Member States, the European Parliament and (sometimes) the public on a variety of issues, including producing an annual report on the functioning of the EU ETS and reporting on how international negotiations relevant to the EU ETS develop.

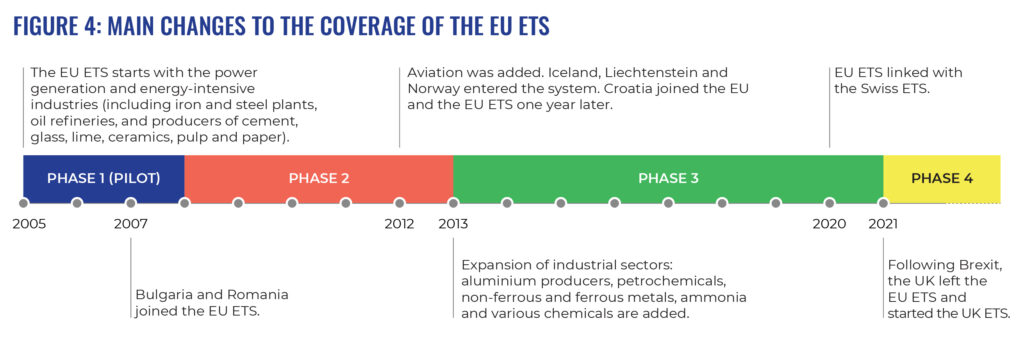

The EU ETS has changed significantly over time since it started in 2005. It has gone through 3 phases, and the fourth phase started in 2021. Over those 16 years the EU ETS was revised several times.

Phase 1 (2005 – 2007) was a pilot phase, implemented to build and test the infrastructure needed to run an ETS, and give business time to understand the system. During this phase nearly all EUAs were handed out for free.

The cap was set by summing up separate caps set by each of the member states (with European Commission oversight) – these were called ‘National Allocation Plans’ (NAPs). These NAPs were set on conservative emission estimates – resulting in a far too large cap and a lot of oversupplied EUAs. As Phase 1 allowances could not be transferred over to Phase 2, the oversupply in Phase 1 was a temporary problem.

Phase 2 (2008 – 2012) continued the use of NAPs, but this time the overall cap was reduced and based on actual emissions data from Phase 1. Around 90% of all emissions under the EU ETS were still handed out for free, but the first auctions were held. International offsets were allowed into the market, and over 1 billion would enter the market by 2012. These international credits, an overgenerous cap and the effects of the financial crisis (when less economic output depressed emissions, without the supply of EUAs being adjusted) led to an enormous oversupply that held EUA prices down til the Market Stability Reserve (MSR) started operating in 2018.

At the start of Phase 3 (2013 – 2020) the EU ETS was changed considerably, building upon the experiences and mistakes from the first two phases. Auctioning became the default method for allocating EUAs, and the electricity sector didn’t receive any free allowances anymore (except limited quantities in some member states as support for modernising their power sectors). A single EU-wide cap was also implemented. International credits were still allowed in, but far less (only around 500 million came in over Phase 3), and they had to be exchanged for EUAs – thereby not making the oversupply any worse.

In 2015 the Market Stability Reserve was created to address the structural oversupply in the market, and 900 million EUAs that had been ‘backloaded’ (i.e. pushed back on the auctioning calendar) earlier in Phase 3 were placed in it. The MSR started actively sucking surplus EUAs out of the market in 2018, and ended a period of very low confidence (and prices) in the ETS.

Phase 4 only started in 2021, and the EU ETS was adapted heavily again before it started. The MRS has been strengthened, and will also cancel EUAs above a certain threshold. Free allocation will be ‘better targeted’ – though approx. 90% of industrial emissions will still be covered by free allocation. The Innovation and Modernization Funds were created, they will invest (respectively) in low-carbon innovation, and energy sector modernisation and just transition.

Note that all these Phase 4 changes are back on the negotiating table due to the ongoing revision of the EU ETS, and starting in 2023 or 2024 (depending on the length of the negotiations) the ETS could be a (slightly or very!) different again.

The scope of the EU ETS has changed over time, with economic sectors being added and countries entering or leaving the system.

The current revision will most likely lead to maritime transport entering the EU ETS – likely both intra-EU shipping and (a part of) voyages to EU ports from third countries and vice versa. The European maritime sector is a large source of climate pollution – responsible for 144 Mt of CO2e emissions in the EU in 2019.

The inclusion of the aviation sector in the EU ETS was first proposed in 2008, with the objective of pricing emissions from all flights within the European Union, as well as flights to and from the EU (i.e. with either the departure or arrival airport located in an EU member state). This quickly sparked a political row as non-EU countries, led by the United States which is home to aviation powerhouse Boeing, engaged in a diplomatic battle to stop this.

When aviation was finally brought under the ETS in 2012, only flights within the European Union and the European Economic Area (EEA) were covered. Long-haul flights will continue to be exempted from EU ETS obligations until 2023, and a new proposal from the Commission might extend the exclusion of such flights beyond this date (the “clock was stopped” repeatedly on bringing international aviation into the EU ETS). This leaves over 50% of the EU’s aviation-related emissions uncovered, as the majority of most EU airlines’ emissions are from long-haul flights that are not covered by the EU ETS. Following the linking between the EU ETS and the Swiss ETS, as well as the Brexit deal, flights from EEA countries to Switzerland or the UK are also covered under the ETS (flights from those countries to EEA countries are covered by the respective national ETS).

In 2016, ICAO, the UN’s aviation agency, agreed on an international carbon offsetting scheme, known as the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA), to compensate for the growth in CO2 from international flights. Despite this scheme being very weak and relying on compensation instead of in-sector reductions, the European Commission proposed to implement CORSIA to cover flights not currently covered by the EU ETS. This would replace the currently planned scope extension scheduled for 2023. From an environmental perspective, this amounts to backsliding compared to the current EU ETS rules. Flights between and within EEA member states would remain covered by the EU ETS.

The stated aim of the EU’s Emissions Trading System is to push cost-effective decarbonisation across key sectors of the EU economy. This implies that the EU ETS should complement the EU’s climate actions by reducing emissions from covered sectors to a level that is in line with the Union’s climate goals. At the end of 2021, the EU ETS was required to decrease the combined emissions of all covered installations by 43%, relative to 2005, by 2030. This target was already reached by the end of 2020, indicating that this was not an ambitious climate target. The falling cap will reach zero by 2058, implicitly setting a longer term pathway for full decarbonisation.

The European Green Deal and the Climate Law raised the EU’s climate ambition, with the EU economy-wide emissions reduction target increased to at least 55% from the previous ‘at least 40%’ (both compared to 1990). This higher ambition needs to be translated into sectoral targets. In July 2021, the European Commission proposed to raise the EU ETS target to a 61% reduction in emissions by 2030 (compared with 2005).

While these higher targets are a step in the right direction, they do not go far enough. Environmental NGOs are demanding that the EU ETS should aim to slash emissions by 70% by 2030, and that the EU should reach climate neutrality a decade ahead of the current official target by 2040 at the latest to stand a chance of keeping global warming below the crucial 1.5°C threshold and shoulder its fair share of climate action.

But is the EU ETS actually succeeding in its bid to decarbonize the sectors it covers?

Total emissions under the EU ETS have fallen considerably. Figure (x) shows how EU ETS total emissions have evolved during Phase 3 (2013-2020). Notice also they have been significantly under the cap over the entire third Phase, so much so that the 40% reduction target for 2030 was already reached in 2020, a full decade ahead of schedule. This is the result, however, not of an abundance of success but of a shortage of ambition.

Moreover, the total reduction in emissions camouflages major differences between sectors. Utilities (electricity and heating) are the key reason why EU ETS emissions have decreased over time. However, industrial emissions have been more or less stagnant since 2013 while aviation emissions have increased (with the notable exception of 2020 when the COVID-19 pandemic resulted in a temporary drop for aviation and industry). The main cause of this discrepancy is that the power sector has had to pay for the vast majority of its allowances since 2013, while aviation and industry still receive massive amounts of units for free, resulting in no strong economic incentive for them to decarbonise their operations.

Figure 6 uses indices to highlight the differences in sectoral emission trends.

Note: aviation and industry emissions are only shown starting in 2013 when the EU ETS expanded to cover aviation and a greater number of industrial sectors. The drop in aviation and industrial emissions in 2020 is due to the temporary economic slowdown caused by the pandemic.

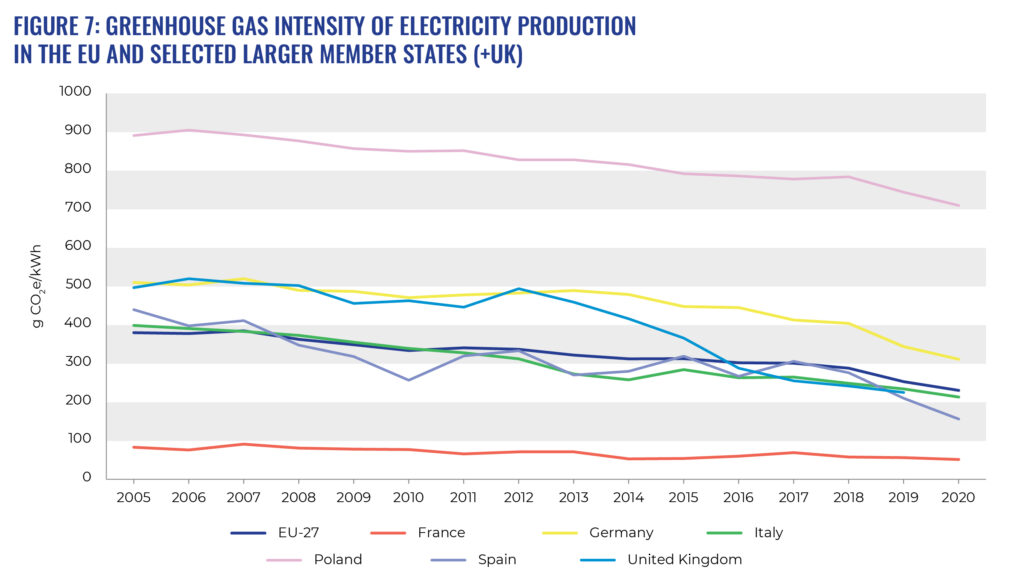

Emissions from electricity and heat production have dropped sharply over the past decade, by nearly 45% since 2011. A key factor underpinning this evolution is the declining quantity of greenhouse emissions required to produce a unity of electricity, which is known as the carbon intensity of electricity production. Figure 7 shows that the carbon intensity of electricity production has decreased steadily since the inception of the EU ETS in 2005, especially in Germany, the UK and Poland, where electricity became relatively cleaner.

But how much of this is due to the EU ETS, and how much due to other factors?

The EU ETS is not the only policy driver affecting the decarbonisation of electricity production. A 2020 study showed that, between 2005 and 2018, the lion’s share of the decrease in emissions from the power sector was due to renewable energy deployment across the EU. The authors noted that the EU ETS did play a role in spurring the transition towards renewable energy, but it was definitely not the main driver. By 2020 that picture had started to change, as energy market data suggest higher carbon prices caused a switch from that dirtiest of fossil fuels, coal, to less dirty gas. Other key drivers of the decarbonisation of the EU power sector include the Energy Efficiency Directive, which has helped tame the demand for energy, the Industrial Emission Directive, which as helped limit non-CO2 air pollutants, and national plans for phasing out coal and lignite in the power mix.

A key lesson can be drawn from this. It is clear that the cost of allowances has not always been sufficient to spur a switch to renewables or less polluting fossil fuels, nor to make coal power plants durably unprofitable. Since 2019, rising carbon prices have had a marked impact on the profitability of coal power plants across the EU. This highlights the fact that carbon prices on their own may not be sufficient and that complementary policies and measures are necessary to truly incentivise decarbonising the power sector.

Note that the EU also imports electricity from neighbouring countries such as Bosnia and Herzegovina and Serbia, including coal-based power that is not included in the numbers and graphs above. The plants in question do not adhere to EU pollution control rules nor do they pay a carbon price. From 2018 to 2020, the Western Balkans exported 25 TWh of electricity into the EU (approximately 0.3% of EU electricity use), amounting to 8% of the total coal-fired power generation in the Western Balkans.

Industrial emissions barely decreased between 2013 and 2019, declining by a paltry 1,3% over that entire period. The main difference between how the EU ETS impacts power and industry is that while the power sector has to buy allowances (at auction or through the secondary market), the industry sector is still receiving most of the EUA it needs for free. More than 95% of industrial climate pollution is emitted at no cost to industry, but at enormous cost to the environment and society, due to energy-intensive industrial sectors being considered at risk of carbon leakage (see sections on Money for nothing and Carbon leakage protection).

With virtually no market incentive, most energy-intensive industries are not strongly committed to investing in cleaner technologies and making the necessary changes to decarbonise. In fact, the current long-term roadmaps presented by the industries themselves, if taken together, represent a mere 18% reduction of greenhouse gas emissions between 2016 and 2050. However, decarbonising energy-intensive industries is possible and a plethora of solutions have already been identified. These include increasing energy savings, scaling up renewable energy deployment and applying circular economy models that, if fully adopted, can put Europe’s heavy industry on a pathway that is compatible with the goals of the Paris Agreement.

Under current legislation, the EU ETS would hand out up to 6.5 billion additional free emission allowances with a market value of about €325 billion between 2021 and 2030 (at EUA prices of €50). This would drop slightly to 5 billion allowances, worth €250 billion, under the European Commission’s Fit for 55 package. This pollution subsidy undermines the EU ETS goal of incentivising the reduction of industrial emissions, including from steel, chemical and cement plants, as well as oil refineries.

In the aviation sector, growth in demand has outpaced increasing efficiency, which means that absolute emissions from this sector continue to rise. Emissions per passenger per kilometer are decreasing slightly every year, but this is of little benefit to the climate when more and more passengers take to the skies. The aviation sector is the only ETS-covered sector where emissions have been consistently increasing. While this trend was interrupted by the COVID-19 crisis, which grounded most planes, it is likely to be temporary and nearly all forecasts predict renewed growth in emissions by approximately 2025.

Some of the medium- to long-term emission reduction opportunities include more efficient and lighter planes, reorganising flight paths and times, and switching from fossil kerosene to alternative sustainable fuels such as green hydrogen or fuels based on renewable electricity (so-called e-fuels). However, all of these measures are only marginal and/or are only at an early stage of development. In the short term, flying less is the only realistic option for reducing aviation emissions. Free allocations to the aviation sector undermine efforts to reduce supply and demand and the urgency to invest in a real zero-carbon transition sooner rather than later.

Finally, it is important to note that only the carbon dioxide emissions from aviation are included in the EU ETS. But this only represents a portion of the total climate impact of the sector. So-called non-CO2 impacts, such as nitrogen oxides and contrails, have an effect that is estimated to be around twice the size of that of CO2. While carbon dioxide stays in the atmosphere for at least centuries, most of the non-CO2 impact would rapidly disappear if planes were grounded today.